In manufacturing and export production activities, the customs settlement report is consistently regarded as one of the most complex and high-risk compliance obligations. Many businesses — from domestic companies filing customs settlement reports for processing operations to those handling settlement reports for export manufacturing — only start paying attention when the deadline is approaching, leading to data errors, discrepancies, and in serious cases, post-clearance tax recovery and penalties. This article will help you understand the regulations, required documentation, and the correct approach to completing your customs settlement report.

I. Overview of the Customs Settlement Report

1. What is a customs settlement report?

A customs settlement report is a consolidated report covering:

- Import of raw materials and supplies;

- Use of raw materials during the production process;

- Export of products manufactured from imported raw materials.

2. Core purposes of the settlement report

- Monitor the use of tax-exempt or tax-deferred raw materials.

- Determine tax obligations arising from surplus materials or materials used for unintended purposes.

- Assess the company’s risk level and legal compliance, informing decisions on post-clearance inspections or in-depth audits.

II. Completing the Settlement Report Under Current Regulations

1. Which businesses are required to submit a settlement report?

Under current regulations, the annual customs settlement report applies to the following entities:

| No. | Type of Business | Specific Activity |

|---|---|---|

| 1 | Domestic enterprise | Performs processing under orders from foreign traders |

| 2 | Domestic enterprise | Manufactures goods for export |

| 3 | Export processing enterprise (EPE) | Executes processing contracts or export manufacturing |

| 4 | Organizations/individuals | Have contracts to outsource processing abroad or to EPEs |

In particular, customs settlement for EPEs differs from domestic enterprises due to the nature of operations within non-tariff zones, businesses should take care to distinguish these when preparing their reports.

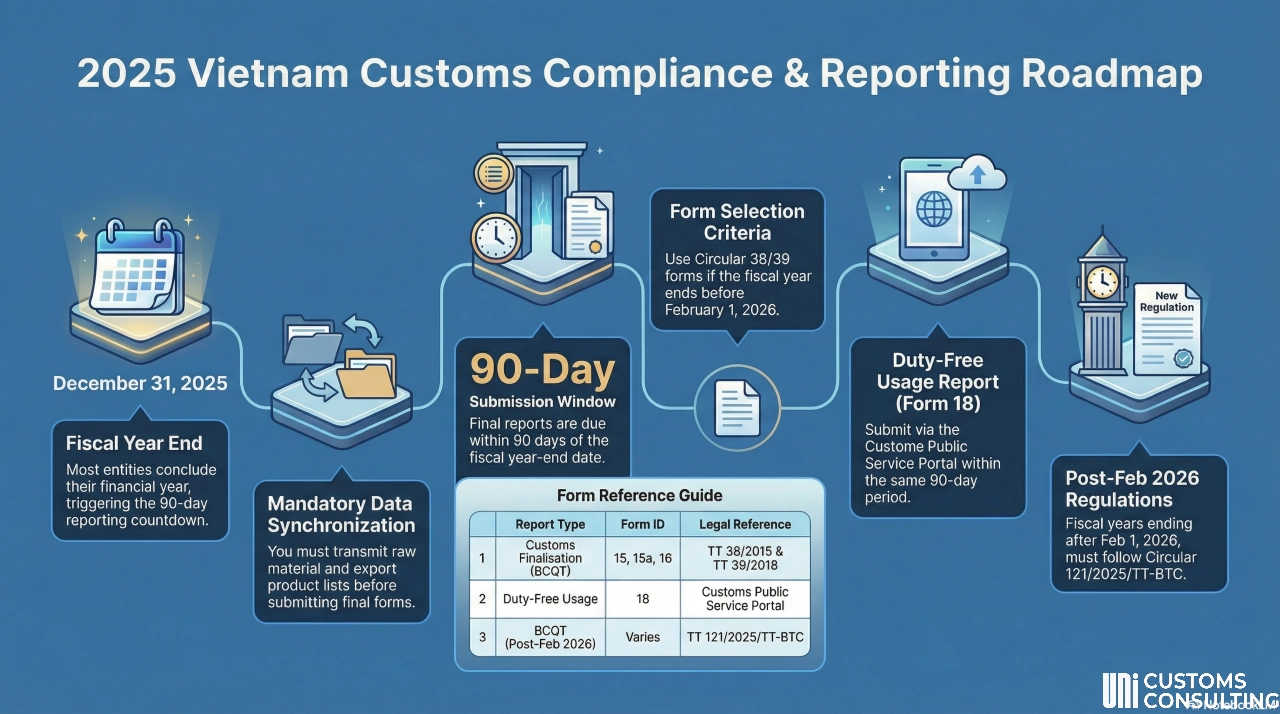

2. Settlement report submission deadline

Deadline: Within 90 days from the end of the fiscal year (31/12/2025).

Applicable Form Templates:

- Fiscal year ending before 01/02/2026: Use forms 15, 15a, 16 per Circular 38/2015 (amended by Circular 39/2018).

- Fiscal year ending after 01/02/2026: Follow Circular 121/2025/TT-BTC.

Technical Note: The list of imported raw materials and exported products must be fully submitted before transmitting Forms 15, 15a, and 16 to avoid system errors.

Report on the Use of Tax-Exempt Imported Goods

- Deadline: 90 days from the end of the fiscal year (31/12/2025).

- Submission: Submit on time using Form 18 through the Customs Authority’s Public Service Portal.

Support: For any questions, please contact the Enterprise Management Division at the Customs Sub-Department where your procedures are handled.

III. Step-by-Step Guide to the Customs Settlement Report

Step 1: Determine the reporting method

The business chooses one of two methods:

- Method 1: Connect the company’s production management system to the customs system to provide real-time transaction data (Form 30).

- Method 2: Prepare and submit the settlement report periodically on an annual fiscal year basis.

Step 2: Consolidate import – export – inventory data from the Warehouse, Accounting, and Import/Export departments

Data consolidation follows the principle of:

- Tracking raw materials and supplies from import → production → export.

- Data is reflected in import – export – inventory format by material code, product code, and declared import type.

Step 3: Determine the actual production norms

The business determines the actual customs production norms — the actual quantity of raw materials consumed to produce one unit of product under the company’s specific production conditions. These norms serve as the basis for:

- Cross-checking against the quantity of imported raw materials.

- Confirming materials were used for their intended purpose.

Step 4: Prepare the settlement report forms

The business prepares and submits the following reports:

- Import – export – inventory report for raw materials and supplies (Form 15 settlement report / Form 15/BCQT-NVL/GSQL)

- Import – export – inventory report for finished products (Form 15a/BCQT-SP/GSQL)

- Actual production norm report for exported products (Form 16/ĐMTT-GSQL)

If the electronic system is unavailable, paper versions (Forms 15/BCQT-NVL/GSQL, 15a/BCQTSP-GSQL, and 16/ĐMTT-GSQL per Appendix V) must be submitted instead.

How to submit production norms and the settlement report

Submission methods:

- Via the customs electronic system.

- Direct paper submission.

Submission locations for paper filing:

- The customs sub-department in the area where the company’s production facility is registered.

- Companies with multiple production facilities may designate one customs sub-department for all settlement report submissions.

Legal basis: Clauses 1 and 2, Article 32 of Circular 121/TT-BTC amending Article 60 of Circular 38/2015/TT-BTC as further amended by Clause 39, Article 1 of Circular 39/2018/TT-BTC.

IV. The Three “Backbone” Reports in the Customs Settlement Package

1. Form 15 Settlement Report – Raw Material Import/Export/Inventory (15/BCQT-NVL/GSQL)

This is the central form in both the customs settlement report for processing operations and export manufacturing settlement, capturing all movements of imported raw materials and supplies during the period. It is prepared based on accounting records combined with actual warehouse tracking data.

Key fields requiring special attention:

| Field | Important Notes |

|---|---|

| Raw material/supply code (Column 2) | Internal codes are permitted but must be consistent with codes declared to customs. If multiple coding systems exist, a conversion table must be available for explanation. |

| Unit of measurement (Column 4) | Must be consistent across all systems and match the unit on the customs declaration; unit mismatches are a common cause of data discrepancies. |

| Quantity imported during the period (Column 6) | Includes all imported raw materials and transferred materials, including goods that have cleared customs but have not yet physically entered the warehouse. |

| Quantity issued for production (Column 9) | Reflects actual raw materials put into production — the basis for cross-checking against consumption norms and output volume. |

| Closing inventory (Column 11) | Must exactly match the physical stock count at the time of period-end closing. |

2. Finished Product Import/Export/Inventory Report (Form 15a/BCQT-SP/GSQL)

This report captures the movement of finished products manufactured from imported raw materials during the settlement period.

Key fields requiring special attention:

| Field | Important Notes |

|---|---|

| Quantity received into inventory (Column 6) | The quantity of fully completed products entering the warehouse, including recovered products from the production process or products received from processing partners. |

| Quantity shipped out during the period (Column 7) | Includes all exported products, products delivered to non-tariff zones, or products returned to the contracting party. |

| Other remarks (Column 11) | Used to explain special circumstances such as change of intended use, destruction, or products used for gifts. |

3. Actual Customs Production Norms – Form 16/ĐMTT-GSQL

The actual customs production norm is the key metric customs authorities use to evaluate whether raw materials were used for their intended purpose. Unlike theoretical engineering norms, the actual norm reflects the real quantity of raw materials consumed to produce one unit of product under the company’s specific operating conditions.

How to calculate the actual production norm:

Actual norm = Total raw materials used ÷ Total products manufactured

This norm includes both the materials incorporated into the product and losses incurred during production, such as scrap and defective items. Businesses are responsible for developing and maintaining technical documentation and must be prepared to justify these figures upon customs request.

Legal basis: Clause 3.b, Article 32 of Circular 121/TT-BTC amending Article 60 of Circular 38/2015/TT-BTC as further amended by Clause 39, Article 1 of Circular 39/2018/TT-BTC.

V. The “Golden” 60-Day Window

One particularly favorable regulation that businesses often overlook is the right to amend and supplement the settlement report.

Under current regulations, within 60 days of the initial submission, if errors are discovered, businesses may resubmit the corrected report without it being considered a procedural violation. This is a safety window for businesses to proactively review and correct figures, reducing risk exposure before customs conducts its follow-up inspection.

Practical note: Many businesses, especially those filing an export manufacturing settlement report for the first time discover norm discrepancies only after submission. Knowing and making use of this 60-day window can prevent significant tax recovery liability.

Legal basis: Clause 3.c, Article 32 of Circular 121/TT-BTC amending Article 60 of Circular 38/2015/TT-BTC as further amended by Clause 39, Article 1 of Circular 39/2018/TT-BTC.

VI. Departmental Responsibilities in the Settlement Process

| Warehouse Department | Accounting Department | Import/Export Department |

|---|---|---|

| Responsible for the accuracy of warehouse receipt/issue documents and physical stock counts; ensures goods are correctly classified and coded per the agreed master list. | Records all inventory movements in full (Accounts 152, 154, 155) and serves as the control function for the legality and validity of documents and invoices. | Handles customs declaration filing and monitors declarations by type; consolidates data from Warehouse and Accounting to produce the complete settlement report. |

VII. Surplus and Deficit Discrepancies in Customs Settlement: What Businesses Need to Know

1. Surplus discrepancy (actual inventory > reported inventory)

The warehouse holds more stock than the figures reported to customs.

Common causes:

- Production norms were set higher than actual consumption.

- More goods were imported than declared, with no supplementary declaration filed.

- Export was declared but goods remain in the warehouse.

Risks:

- Customs may suspect inaccurate or fraudulent reporting.

- The business may be flagged for post-clearance inspection.

What businesses should do:

- Review and recalculate actual production norms.

- Audit all import declarations.

- Prepare explanatory documentation covering reasonable wastage and tolerances.

2. Deficit discrepancy (actual inventory < reported inventory)

The warehouse holds less stock than the figures reported to customs.

Common causes:

- Goods lost or damaged without proper documentation.

- Tax-exempt raw materials used for domestic sale.

- Scrap and defective products destroyed without following proper procedures.

- Actual customs production norms set lower than actual consumption rates.

Risks:

- Recovery of import duties and VAT.

- Administrative fines and late payment penalties.

What businesses should do:

- Conduct regular physical stock counts.

- Prepare complete documentation for damaged or lost goods.

- When selling domestically, file a change-of-use declaration (Form A42) promptly.

VIII. Scrap and Defective Products: Understanding the Rules to Avoid Mistakes

In the context of export manufacturing settlement reports, scrap and defective products are an unavoidable reality — but they must be handled in accordance with regulations.

If sold or consumed domestically:

- Customs procedures are not required.

- However, domestic tax declarations and payments still apply.

If destroyed:

- Must be carried out under customs supervision.

- Full documentation must be retained: destruction minutes, waste disposal contracts.

If returned to the contracting party:

- Process under declaration type B13.

Accounting note: Recovered scrap must be fully recorded in the accounting system and reconciled with the settlement report to prevent discrepancies.

IX. UNI’s Customs Settlement Report Services

The customs settlement report — whether for processing operations, export manufacturing, or EPE settlement — is a high-stakes obligation requiring absolute accuracy and deep knowledge of the regulatory framework. A single error can trigger tax recovery, penalties, or significant financial assessments.

UNI supports businesses from initial data collection through regulatory review, cross-checking consistency between customs, accounting, and production records, to preparing settlement reports in the correct format and on time — ensuring full compliance with customs authority requirements and minimizing the risk of post-clearance penalties and tax recovery.

>>>> Related service: End-to-end customs declaration

📞 Contact UNI Customs Consulting for a free consultation

📧 Email: uni@eximuni.com

📱 Hotline: (+84) 24-7308-7988 (Hanoi) | (+84) 28-7301-8910 (HCM)