Converting to Authorized Economic Operator (AEO) status is becoming an inevitable trend that helps import-export enterprises optimize customs procedures and enhance competitiveness.

In the context of the newly issued Decree 167/2025/ND-CP, which amends regulations related to conditions for enterprises to enjoy AEO status, understanding the new standards and conversion process has become more important than ever for enterprises wanting to take advantage of customs clearance benefits and customs inspection exemptions.

1. What is an Authorized Economic Operator (AEO)?

a. How is an Authorized Economic Operator (AEO) understood?

Authorized Economic Operator (AEO) is a program initiated by the World Customs Organization (WCO), applied to import-export enterprises that demonstrate capability and good compliance with supply chain security regulations.

In Vietnam, AEO enterprises are understood as export and import enterprises recognized by customs authorities as priority enterprises.

(According to Circular 72/2015/TT-BTC)

In general, when an enterprise meets the standards of the AEO program, customs authorities will confirm that this enterprise can perform declarations and clearance with special preferential treatment.

b. Authorized Economic Operator (AEO) in Vietnam

AEO enterprises are included in the trusted list of Vietnam Customs and signatory countries. In Vietnam, there are three types of priority enterprises:

- Priority for all import-export goods;

- Priority for agricultural products, seafood, textiles, leather and footwear;

- High-tech enterprises prioritized for importing raw materials and auxiliary materials and exporting high-tech products.

Being recognized as AEO helps enterprises affirm their reputation and supply chain management capabilities, while opening up many opportunities for cooperation with international trading partners.

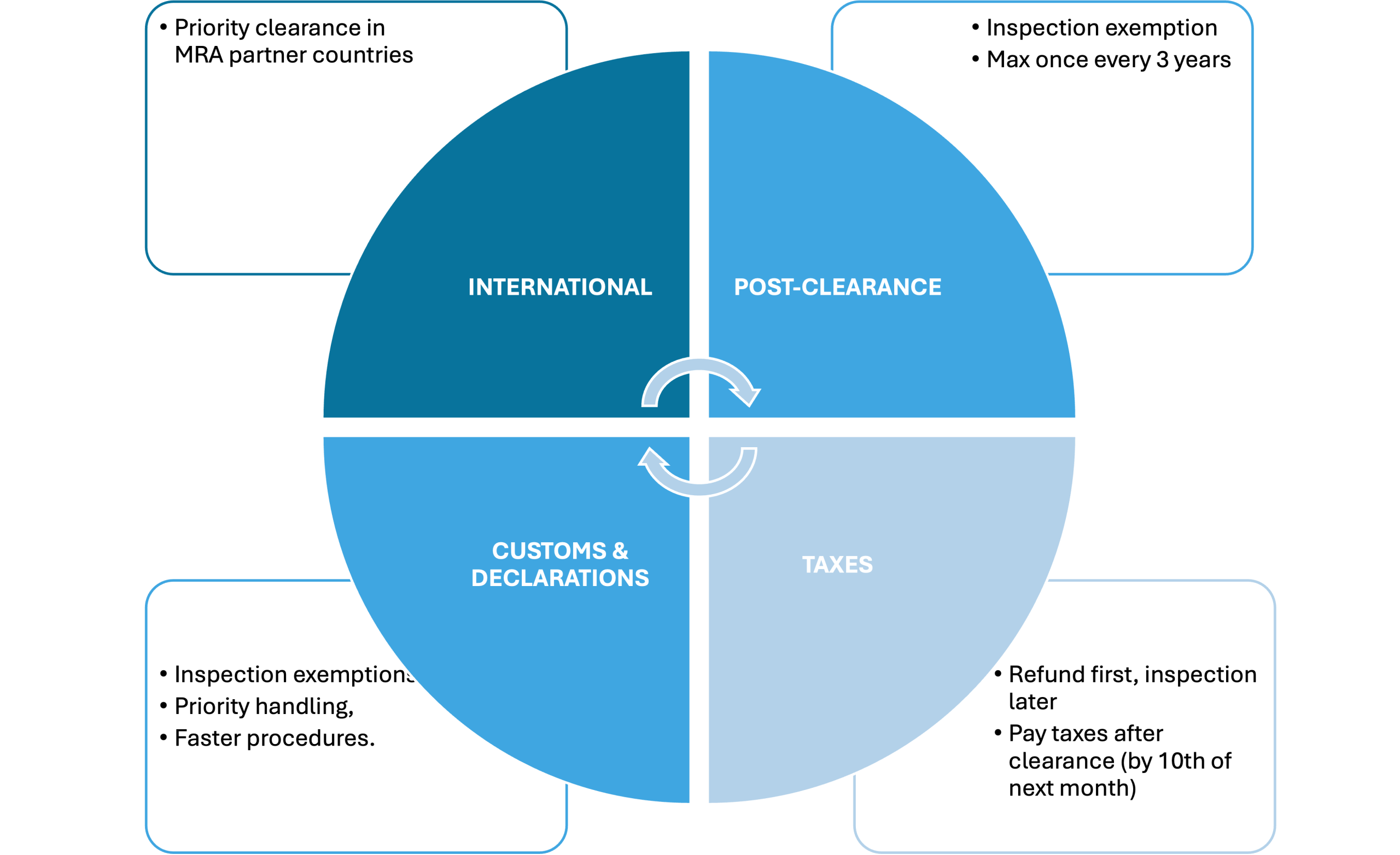

2. Benefits of Converting to Priority Enterprise?

Being recognized as an Authorized Economic Operator (AEO) brings many practical benefits to import-export enterprises. Below are the main benefits that AEO enterprises typically enjoy:

a. In customs procedures and specialized inspections

a. In customs procedures and specialized inspections

Converting to AEO enterprise helps businesses enjoy many priorities in customs procedures and specialized inspections, specifically:

Document inspection exemption and physical goods inspection exemption. AEO enterprises are exempt from document inspection and physical goods inspection, except in cases of violation signs or random inspection (random inspection rate maximum 0.5% for non-EPE enterprises).

(According to Article 5 of Circular 72/2015/TT-BTC)

Priority in specialized inspections: Imported goods can be moved to storage warehouses while waiting for specialized inspection results (except when inspection at border gates is required) and priority sampling.

(According to Article 8 of Circular 72/2015/TT-BTC)

Priority in on-site import-export procedures: For raw materials, components, and spare parts purchased from bonded warehouses for production, AEO enterprises are entitled to:

- Import first, declare customs later within maximum 30 days.

- Register declarations at 1 most convenient Customs Office.

- No physical goods inspection, only document inspection for delivery and receipt.

(According to Article 86.6 of Circular 38/2015/TT-BTC)

Additionally, enterprises are given priority by customs authorities in the order of customs procedures. In case AEO enterprises encounter difficulties, Customs provides written explanations within 8 working hours from the time problems arise. Customs authorities, ports, and warehouses prioritize goods delivery and receipt procedures first, priority inspection and supervision first. Priority for enterprises to conduct goods viewing procedures first, goods sampling first when requested. Priority for physical goods inspection using scanning machines before Customs conducts random goods inspection.

Note: For each delivery and receipt, both the exporter and importer must store documents proving goods delivery and receipt, including: commercial invoices or VAT invoices or sales invoices, internal warehouse release and transport slips, etc.

b. When clearing incomplete declarations and priority in customs procedure order

AEO enterprises enjoy flexible mechanisms when making customs declarations.

In some cases, priority AEO enterprises may be allowed to clear incomplete declarations, with the condition of supplementing documents after goods have been cleared within 30 days.

(According to Article 6 of Circular 72/2015/TT-BTC, amended by Circular 07/2019/TT-BTC)

c. Priority tax procedures

AEO enterprises are given priority in tax processing procedures. Specifically, regarding tax refunds:

- Enterprises receive tax refunds first, then Customs conducts document inspection.

- Tax authorities issue tax refund decisions within no more than 01 working day from receiving complete documents.

Tax payment deadline for import-export goods:

AEO enterprises are allowed to pay taxes after goods clearance, no later than the 10th day of the following month.

(Article 1.4 of Circular 07/2019/TT-BTC and Article 9.2 of Import-Export Tax Law 2016)

d. Post-clearance inspection exemption

During post-clearance inspection processes, AEO enterprises are prioritized to be exempt from post-clearance inspection rounds if not necessary (except when there are signs of legal violations).

Accordingly, customs authorities conduct inspections at declarant premises no more than 1 time in 3 consecutive years based on the date of AEO enterprise recognition (except when there are signs of legal violations).

(According to Article 11 of Circular 72/2015/TT-BTC)

Overall, thanks to these benefits, AEO enterprises can accelerate import-export activities, enhance reputation with customs authorities and trading partners. Especially, when Vietnam signs Mutual Recognition Agreements (MRA) on AEO with many countries, priority enterprises also enjoy similar clearance benefits when exporting to those markets.

3. Conditions for AEO Recognition

To be considered for priority enterprise status, enterprises must meet a series of strict conditions regarding legal compliance, financial capacity, and internal management processes.

Updated according to the newly issued Decree 167/2025/ND-CP, the basic criteria include:

a. Tax-customs law compliance:

In the most recent 2 consecutive years (24 consecutive months calculated to the application submission date), enterprises must not violate the following acts:

- Tax evasion; smuggling; production, trading of prohibited goods or illegal transportation of goods and currency across borders

- Other violations with fines exceeding the authority of Customs Team Leaders.

(Article 1.5.a of Decree 167/2025/ND-CP)

b. Good compliance with accounting and auditing laws:

Enterprises wanting to become Authorized Economic Operators (AEO) must:

- Apply Vietnamese accounting standards issued by the Ministry of Finance.

- Annual financial statements audited by qualified audit companies, with unqualified audit opinions (no exceptions).

According to new regulations in Decree 167/2025/ND-CP, regarding assessment scope:

- Assessment scope is 02 years (24 months) continuous before AEO application submission.

- For newly established enterprises with less than 1 financial year, assessment will be from business registration date to application time.

(Article 1.5.b of Decree 167/2025/ND-CP)

c. Import-export turnover

Basically, conditions regarding import-export turnover for AEO enterprise registration remain at levels equivalent to old regulations, specifically:

- Minimum turnover for import-export enterprises: 100 million USD/year.

- Minimum turnover for enterprises exporting goods manufactured in Vietnam: 40 million USD/year.

- Enterprises exporting agricultural products, seafood produced or cultivated in Vietnam: 30 million USD/year.

New regulations in Decree 167/2025/ND-CP have abolished previous regulations for Customs Procedure Agents: “d) Customs Procedure Agents: number of customs procedure declarations per year reaching 20,000 declarations/year.”

(Article 1.5.d of Decree 167/2025/ND-CP)

d. Internal management system

Unlike old regulations, the newly issued Decree 167/2025/ND-CP has specified very clear criteria related to internal management systems. Specifically:

Internal control system requirements (operational management):

- Document storage: Maintain complete import-export documents, materials, and data and provide promptly to customs when requested.

- Internal supervision: Self-assess, review departmental activities; internal training on supply chain security and response measures when incidents occur.

- Risk management: Prevent and handle goods security abnormalities; remedy errors and violations according to recommendations or conclusions from state agencies.

- Financial control: Ensure financial capacity to fulfill tax obligations on time when prioritized for tax payment deadlines; no tax debt at assessment time.

Enterprises need to establish and maintain internal control systems to ensure supply chain security and safety, including:

- Goods security: Measures to protect original goods condition and control access.

- Transport security: Measures to ensure security throughout goods transportation.

- Work area security: Area division and separation; access control; 24/7 surveillance camera installation at gates, entrances, storage areas (minimum 3-month data storage).

- IT security: Ensure data confidentiality, storage, recovery, and proper system use.

- Personnel security: Background checks for personnel in important positions (CEO, Director, Chief Accountant, Import-Export Department Head, Warehouse, Security) with no criminal record; employee identification; prevent resigned employees from accessing systems.

- Trading partner security: Contracts with partners (transport, customs agents, suppliers…) must include security clauses to ensure information and goods accuracy and integrity.

(Article 1.5.c of Decree 167/2025/ND-CP)

4. Detailed Process for Converting to AEO

The AEO enterprise recognition process in Vietnam is regulated as follows:

a. Process diagram:

b. Specific main steps include:

Step 1: Application submission

- Enterprise prepares application according to new Decree 167/2025/ND-CP.

- Submit to Customs Department for consideration and recognition.

Step 2: Document assessment

- Customs Department assesses application within 5 working days from receiving complete application, comparing information with AEO conditions.

- If conditions are not met, within 15 days from assessment completion, Customs Department responds in writing, clearly stating reasons. If conditions are met, proceed to actual assessment.

Step 3: Actual assessment

- Conduct post-clearance inspection at enterprise premises, maximum 10 working days from inspection start.

- If enterprise was inspected post-clearance in the last 24 months, will base on those results and supplementary actual assessment.

- For enterprises operating less than 2 years, no post-clearance inspection but only actual assessment within maximum 10 days.

Step 4: Decision issuance Within 15 days from actual assessment completion or inspection result processing:

- If conditions are met, Customs Department Director issues AEO recognition decision, valid for 03 years.

- If not achieved, issue written response, clearly stating reasons.

- In complex cases, deadline may extend but not exceed 30 days.

5. UNI Customs Consulting – Trusted Partner in AEO Conversion

UNI Customs Consulting (UNI Consulting Co., Ltd.) is a professional unit in the field of Authorized Economic Operator (AEO) conversion in Vietnam. With many years of experience supporting enterprises in optimizing customs procedures and enhancing import-export efficiency, we have built a professional consulting team and effective working processes, bringing practical value to customers.

a. Experienced expert team

We gather a team of customs experts, lawyers, and import-export personnel with many years of industry experience.

Our team has deep understanding of customs law regulations, import-export taxes, and regularly updates the latest changes from Vietnam Customs Department as well as international practices. Thanks to this, we can provide optimal and most suitable solutions for each enterprise.

b. Comprehensive consulting services

UNI Customs Consulting provides comprehensive solutions for AEO conversion and customs procedures, including:

- AEO conversion consulting: Supporting enterprises to achieve AEO certification, optimizing clearance processes and enjoying customs benefits

- Management system assessment and improvement: Review and upgrade internal management systems to meet AEO standards

- Customs procedure consulting: Guidance and support in completing documents, ensuring customs law compliance

- Legal support and compliance monitoring: Resolving issues, ensuring AEO certification maintenance.

>>>> Related service: EPE ENTERPRISE & PRIORITY ENTERPRISE CONVERSION

Reference documents:

- Decree 08/2015/ND-CP.

- Decree 167/2025/ND-CP amending and supplementing Decree 08/2015/ND-CP.

- Circular 72/2015/TT-BTC.

- World Customs Organization website. Link.

📞 Contact UNI Customs Consulting for free consultation:

📧 Email: uni@eximuni.com

📱 Hotline: +(84) 908-535-898 (Vietnamese) | +(84) 902-927-767 (Korean)